Categories

Agents, BuyersPublished June 12, 2026

Renting vs. Buying in Cumberland County: Let’s Do the Math (It’s Not as Scary as It Sounds)

Renting vs. Buying in Cumberland County: Let’s Do the Math (It’s Not as Scary as It Sounds)

The renting vs. buying debate has been going on longer than the internet, and somehow it still manages to stress people out. Team Rent says flexibility! Team Buy says equity! And meanwhile, a lot of people just keep doing whatever they’re already doing because making a change feels overwhelming.

So let’s skip the debate and just look at the numbers — specifically in Cumberland County, where the math actually has a lot to say. We’ll break it down simply, throw in some real-world context, and help you figure out which path makes more sense for where you are right now.

The Core Question: Where Does Your Money Go?

When you rent, your monthly payment covers your housing — and that’s it. At the end of your lease, you have no ownership stake, no equity built, and nothing to show for the thousands of dollars you’ve paid. Your landlord, on the other hand, has been building wealth with your rent check.

When you buy, your monthly mortgage payment is doing two things: covering the

interest on your loan (the cost of borrowing) and paying down your principal (which

builds equity). Over time, an increasing portion of every payment goes toward equity

rather than interest. You’re essentially paying yourself.

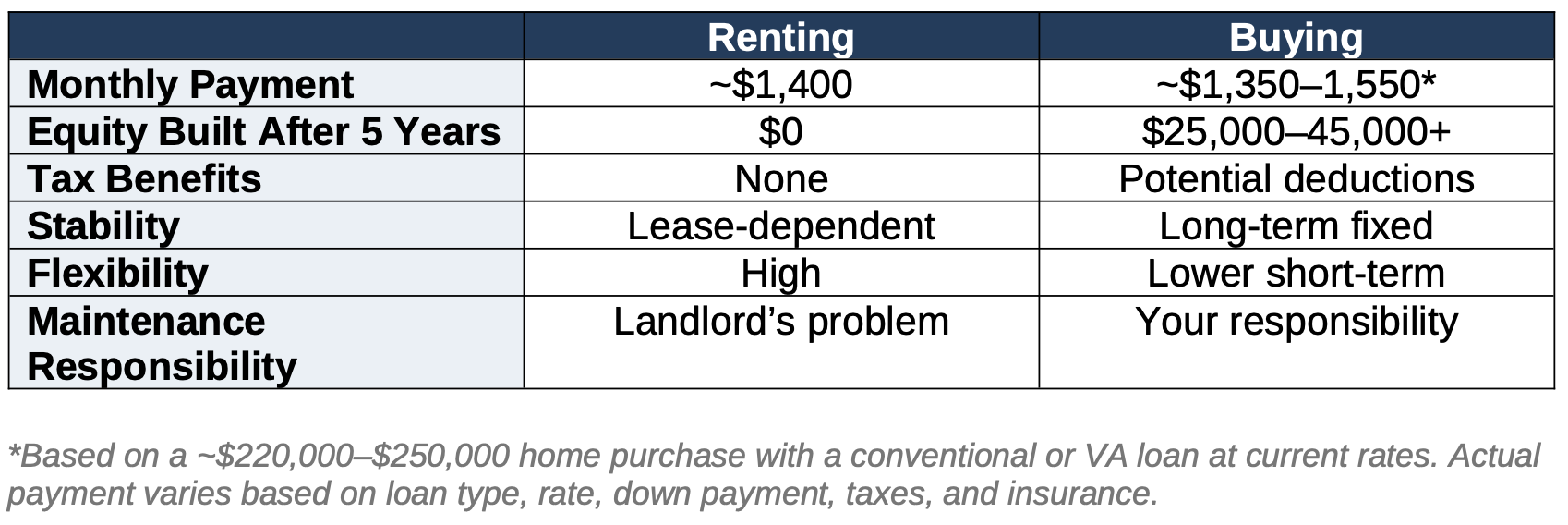

A Side-by-Side Look at the Numbers in Cumberland County

Let’s use a realistic local example. Say you’re currently renting a 3-bedroom home in

the Fayetteville area for around $1,400/month. Here’s how that stacks up against buying

a comparable home:

The Case for Buying in Cumberland County Right Now

Here’s what makes the math particularly interesting in this market: home prices in Cumberland County are still well below the state average, which means your entry point is lower than in most of North Carolina. That translates to lower monthly payments and a more manageable path to homeownership.

Buying makes strong financial sense when:

•You plan to stay in the area for at least 3–5 years

•Your monthly mortgage payment would be comparable to (or less than) what you’re paying in rent

•You have a stable income and a manageable debt-to-income ratio

•You’re eligible for a VA loan — in which case, the no-down-payment benefit makes buying even more accessible

The Case for Renting (Yes, We’re Saying It)

Look, we’re not here to push homeownership on people who aren’t ready for it. There are absolutely situations where renting is the smarter move:

•You’re new to the area and not yet sure where you want to put down roots

•You’re on a short PCS assignment and will likely be moving again within 1–2 years

•Your credit or savings aren’t quite where they need to be yet

•Your life circumstances are in flux — job change, family changes, major transitions

Renting intentionally while you prepare to buy is a perfectly valid strategy. The key word is intentionally — know why you’re renting, have a plan, and don’t let inertia keep you renting indefinitely when buying would serve you better.

So… Which Is Right for You?

Honestly? The answer depends on your specific financial situation, your timeline, and your goals. What we can tell you is that for many renters in Cumberland County right now, the gap between a monthly rent payment and a mortgage payment is smaller than they think — and the long-term difference in wealth-building is enormous.

The best way to find out where you stand is to run your actual numbers with someone who knows this market. No pressure, no commitment — just a clear-eyed look at what’s possible for you right now.

📊 Want to run your own numbers? Reach out to the Welcome Home Team and let’s figure out which path makes the most sense for you.

Brian O'Connell

Owner | Welcome Home Team | Keller Williams Realty

or another way